Count me in!

Stay up to date with the latest news, announcements, and articles.

Cryptocurrency mining has long been a way to earn digital coins, but for 2024, it’s also emerging as a surprisingly effective tool for managing your tax bill. As governments worldwide tighten their grip on crypto regulation, miners are discovering that strategic tax planning can protect their earnings as well as help reduce tax liabilities.

Let’s explore how savvy miners can turn crypto mining into a tax-smart venture and direct crypto mining tax deductions in their own favor.

If you’re a crypto miner — or thinking about becoming one — you’ve probably noticed that governments are paying a lot more attention to cryptocurrency. In 2024, this translates into stricter tax obligations for miners and a potentially more complex and structured crypto mining income tax:

But while a tax oversight of cryptos may seem intimidating, it also creates opportunities for miners who understand the tax rules. Thus, you can keep more of your hard-earned crypto if you comply and, more importantly, leverage deductions.

Crypto mining isn’t just about plugging in rigs and watching coins roll in — it’s a business with serious investments, testing challenges, and, now, specific tax implications. That wasn’t a thing, yes, but we must adapt in time. Here’s what you need to know about the crypto mining business tax specifics:

These financial elements must be figured out if you want to make sure you’re not leaving money — or deductions — on the table. We’ll help you out, read on.

Of course, new taxations do not make crypto mining all just about overcoming financial challenges — on the flip side of things, we get a slew of major tax benefits that could be leveraged to balance out the tax coverage situation in your favor. So if you play your cards right, you can cut your tax bill and boost your net earnings.

Now, let’s see the exact ways how you can do that.

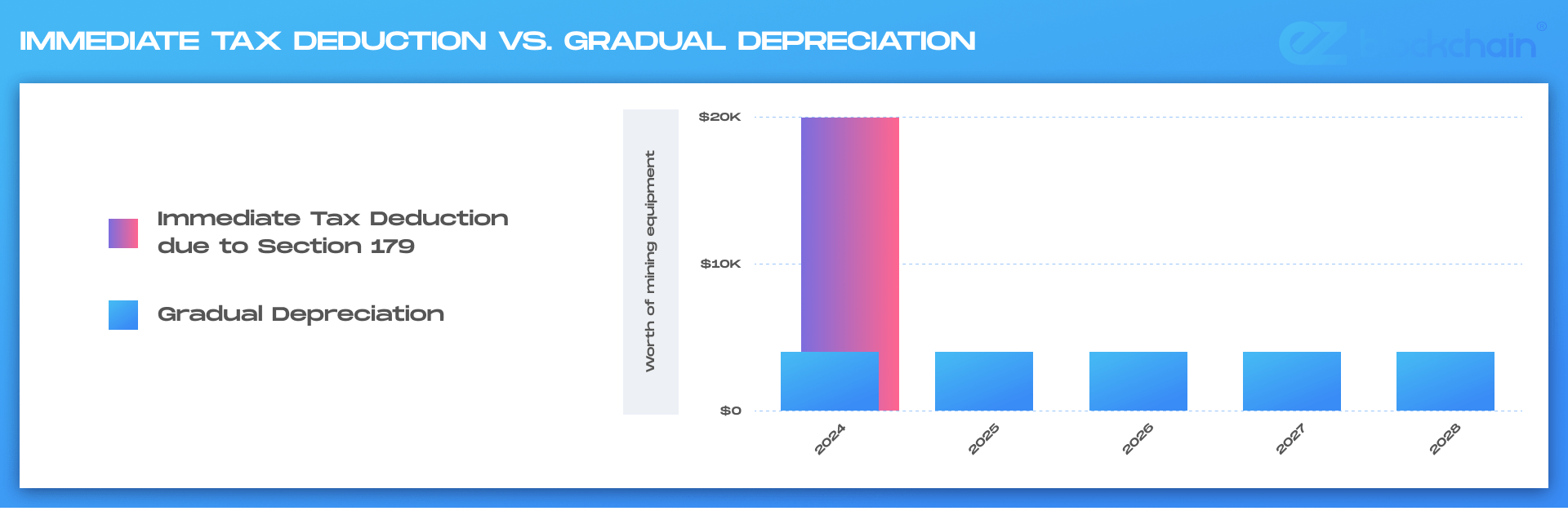

Mining equipment doesn’t come cheap, but the tax code lets you deduct its cost over time. Depreciating your rigs allows you to offset the expense year by year.

Section 179 of the U.S. tax code provides a powerful tool for crypto miners looking to maximize their tax savings. Designed primarily for small to medium-sized businesses, Section 179 gives businesses immediate deduction — instead of depreciating your mining rigs over a 5-year schedule (the typical lifespan for this type of equipment), Section 179 allows you to claim the entire cost upfront.

Example: If you purchase $20,000 worth of mining equipment in 2024 and it qualifies for Section 179, you can deduct the full $20,000 from your taxable income that same year.

Running a mining setup comes with plenty of expenses, many of which are tax-deductible. Some examples include:

Careful documentation is your everything here — tax authorities always require detailed proof of expenses. So save those receipts and keep detailed records of every expense and crypto mining tax write-off tied to your mining activities.

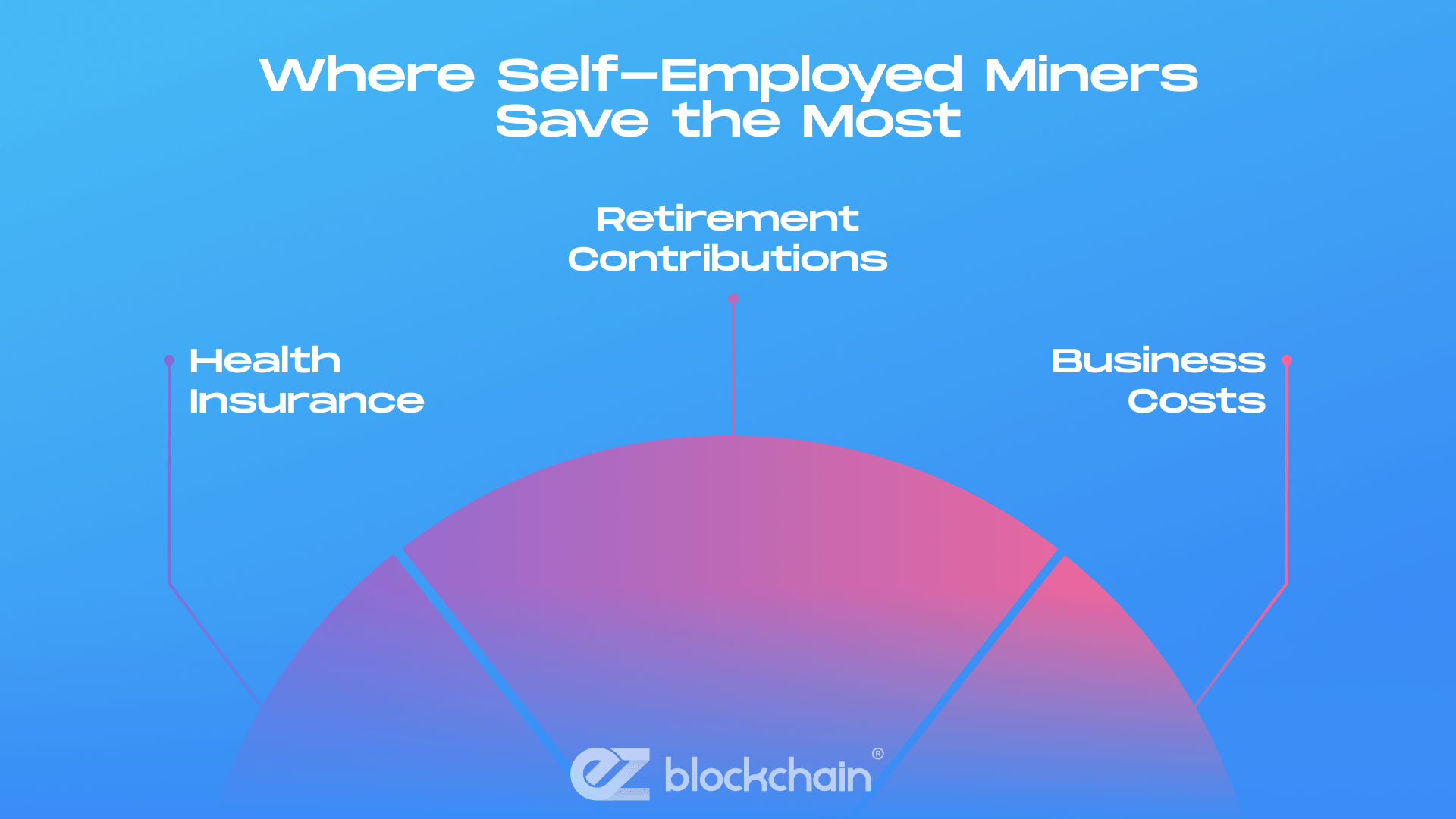

If you’ve turned mining into a business, the tax perks get even better. As a self-employed miner, you may be eligible to deduct:

Key insight: Classifying your operation as a business rather than a hobby can enable a range of extra deductions, but it comes with greater reporting responsibilities as well.

As the tax environment around crypto continues to get more structured and complex, staying compliant is non-negotiable. For profitable crypto mining in 2024, here are some critical crypto mining tax treatment principles and rules miners should keep in mind:

Failing to follow these rules will result in audits, penalties, and other possible costly headaches. So the easiest way to protect your earnings is to stay informed and compliant across the board.

Crypto mining can be quite profitable, but in order to actually keep those profits, one must figure out how to calculate one’s tax advantages. Here’s what you should analyze:

Staying within the bounds of the law while retaining more of your hard-earned crypto assets is possible if you keep things maintained.

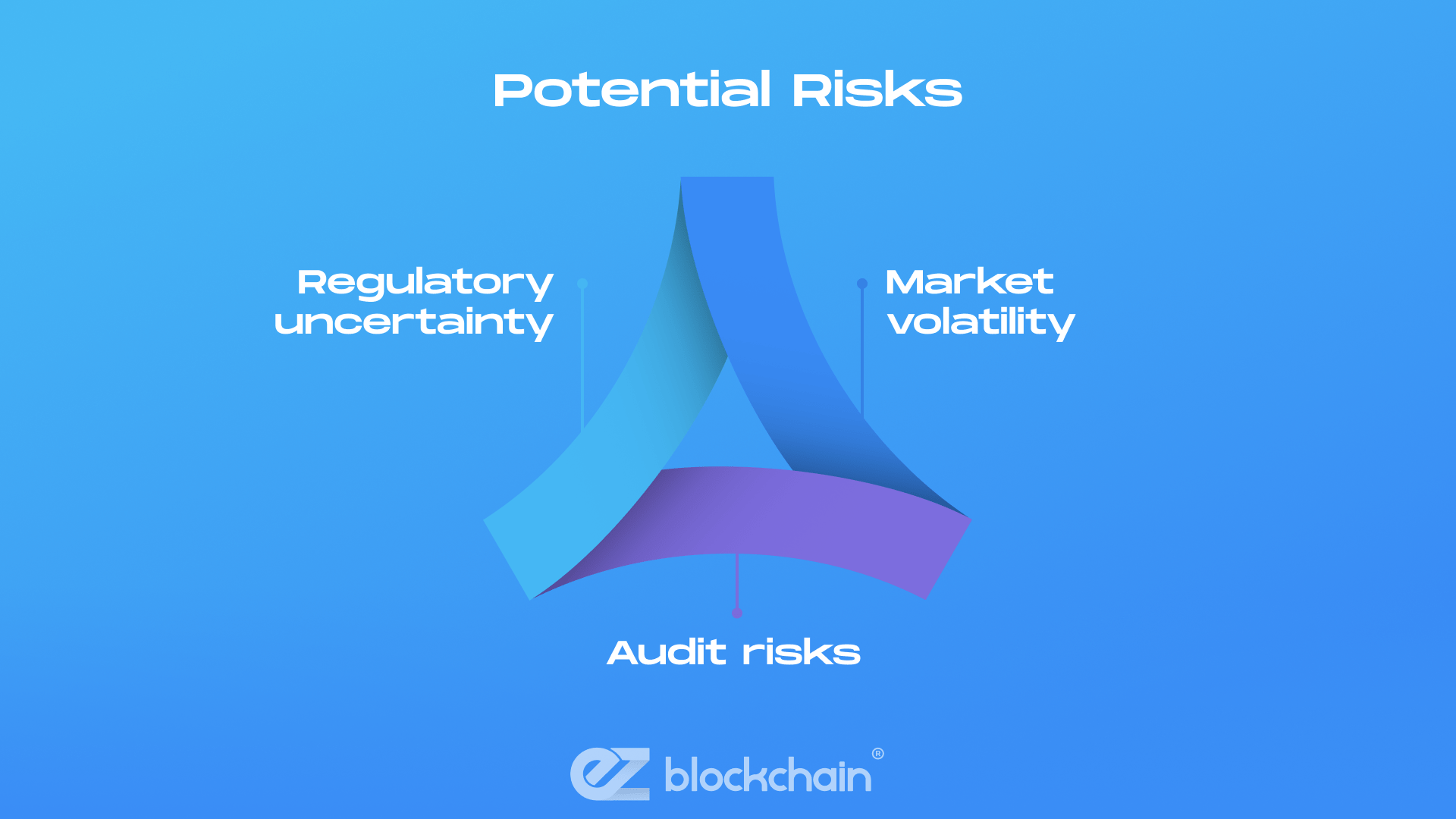

Crypto mining isn’t without its risks, some of which directly affect its taxation principles. Here are a few challenges to be aware of — and how to mitigate them:

Pro tip: Working with a tax professional familiar with cryptocurrency is one of the best ways to ensure compliance and optimize your tax strategy.

With the ever-growing electricity costs and stricter tax regulations, mining crypto in 2024 may not be for everyone. Before jumping in, consider:

For those willing to put in the effort, crypto mining can offer both financial rewards and meaningful tax advantages.

In 2024, crypto mining is about more than just earning cryptocurrency — it’s about being strategic with your finances. By taking advantage of tax deductions for equipment, operational costs, and self-employment, miners can offset rising financial obligations and tax burdens in 2024, boosting profitability at the same time.

Success in this space depends on staying informed, compliant, and reactive. With careful planning and the right approach, mining can be both lucrative and tax-efficient.

So, if you’re ready to mine smarter and not harder, starting out with crypto mining in 2024 might just be your shot. We’ll help you start on your journey — the specialists at EZ Blockchain will guide your tax deduction efforts.

Contact us to discuss the best-fitting opportunities that you can leverage today.

Fill out a form and our bitcoin mining expert will contact you.

FREE CONSULTATIONFill out a form and our bitcoin mining expert will contact you.