Count me in!

Stay up to date with the latest news, announcements, and articles.

At its core, tax loss harvesting realizes capital losses by selling assets at a loss and using those realized losses to offset taxable capital gains (and in certain cases ordinary income). In the U.S., capital losses first offset capital gains dollar-for-dollar; any remaining net capital loss can offset up to $3,000 of ordinary income per year for individual filers, with excess losses carried forward indefinitely .

Because U.S. federal tax treats cryptocurrency as property (not currency or a security for most purposes), sales, exchanges, and dispositions of crypto generate capital gain or loss events that are reported on Form 8949 and Schedule D. That property designation is the legal foundation that allows crypto TLH today .

Two operational consequences flow from these rules:

In practice, TLH converts ephemeral paper losses into a quantifiable tax asset recorded on your return, an asset you can spend in future tax calculations, year after year.

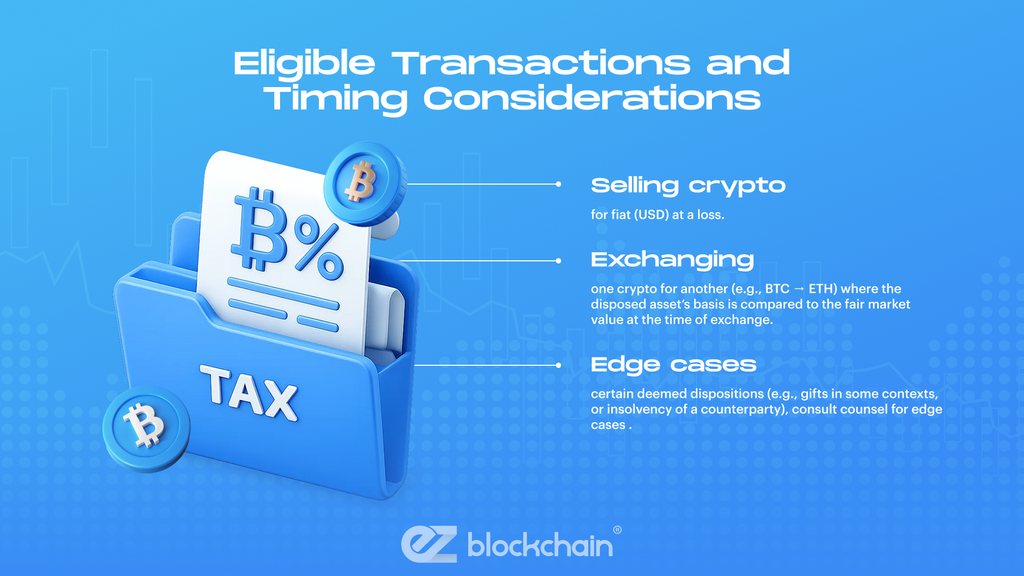

Not every transaction produces a usable tax loss; you must execute a realized disposition. Eligible events typically include:

Timing considerations are crucial. Unlike many securities, the traditional 30-day “wash sale” rule that disallows losses when you repurchase a “substantially identical” security within ±30 days currently applies to securities and not to property categories treated as non-securities.

Because the IRS treats crypto as property, the wash-sale prohibition has historically not applied to cryptocurrencies, meaning taxpayers could, in many cases, sell at a loss and immediately reacquire the same token without auto-disallowance of the loss. That said, analysts and tax advisors caution that legislative or IRS rule changes could alter that status, so treat the existing gap as opportunistic but potentially ephemeral .

TLH requires (a) a genuine sale or disposition recorded on-chain/exchange, and (b) careful timing, the current regulatory environment permits close re-buys, but that gap may close with future rulemaking.

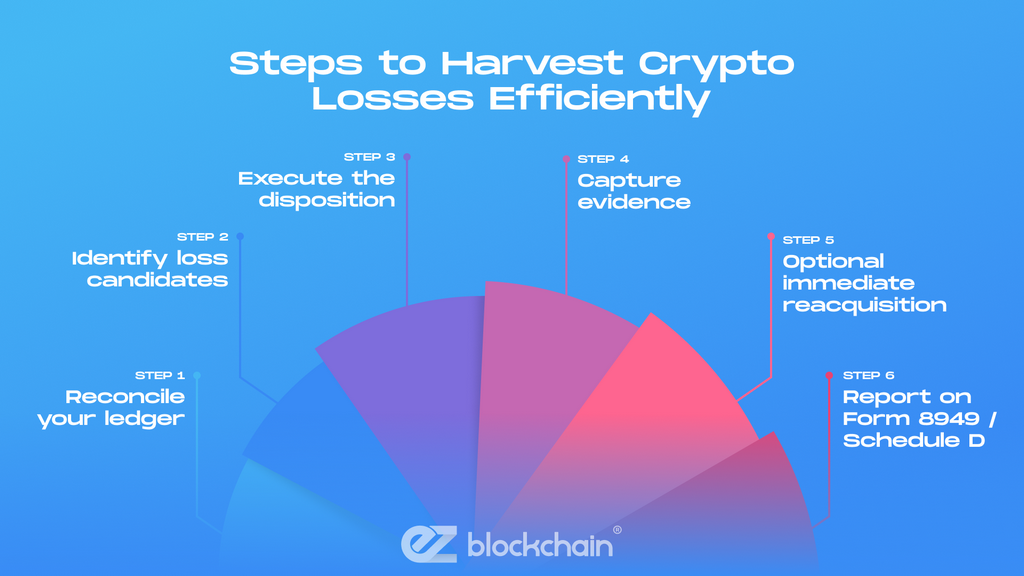

Below is an operational workflow you can plug into your year-end or intra-year tax process. Treat it as a checklist for execution and documentation.

That procedural loop, reconcile, identify, sell, document, and report, is the repeatable core of tax loss harvesting. Automation and disciplined record retention convert TLH from an ad-hoc tactic into a repeatable tax optimization.

Mechanically, realized losses offset realized gains in the same tax year. If you harvested losses beyond your realized gains, apply the $3,000 annual offset rule for ordinary income and carry forward any remaining loss. Keep in mind holding-period classification (short-term vs long-term), matching short-term losses against short-term gains first preserves the more favorable long-term gain treatment where possible.

The IRS forms (Form 8949 and Schedule D) require you to categorize and subtotal these buckets before deriving the net taxable outcome.

Smart harvesting is not only about maximizing the nominal loss. It’s about sequencing disposals so that you preserve the tax character (short vs long) of gains you wish to shelter.

The IRS expects robust documentation. Required and recommended items include:

Software can automate much of this work, but do not rely solely on vendor screenshots if you might need to substantiate items in an audit. The IRS has been explicit: taxpayers must report digital-asset transactions and answer the digital-asset question on Form 1040; be prepared to show supporting source data.

Treat your TLH packet as an audit bundle. If you would not be comfortable sending it to a revenue agent, it is not sufficiently documented.

Key dangers to manage:

TLH is a tax optimization tactic that introduces operational overhead and regulatory risk; its net benefit must be modeled against these costs before execution.

Several tax-tech vendors integrate exchange APIs and chain analytics to produce Form 8949 outputs and audit-ready workpapers. Leading options include CoinLedger, Koinly, CoinTracker, and TokenTax, each supports multiple exchanges, NFT/DeFi transaction types, and carryforward loss tracking. Evaluate vendors on (a) chain/exchange coverage, (b) reconciliation accuracy, (c) audit documentation exports, and (d) rule-update cadence .

A good tax-tech stack reduces manual errors and creates the immutable audit trail the IRS expects, indispensable for scalable TLH practices.

TLH is not a substitute for sound allocation. Harvesting should be integrated into an investment plan that prioritizes risk management, rebalancing policy, and liquidity needs. Over-harvesting (selling high-quality core holdings solely for tax reasons) can impair long-term returns; conversely, selective harvesting of tactical positions or small, underperforming tranches can both reduce near-term tax bills and preserve strategic allocations. Use TLH as portfolio maintenance, not as the primary alpha engine.

The optimal approach blends tax optimization with investment discipline, harvesting opportunistically, but letting your strategic asset allocation drive major decisions.

In the UK, HMRC treats crypto disposals as capital transactions and allows capital losses to offset gains; losses carried forward must generally be registered within specified timeframes and used against future gains. The UK has also ramped enforcement and data collection on crypto holdings, increasing the operational risk of non-compliance. Other OECD jurisdictions vary in detail (some treat certain crypto activity as income rather than capital gains), which affects TLH applicability and timing. Always consult local guidance before applying U.S. TLH playbooks abroad .

TLH is jurisdictionally sensitive. A U.S.-centric method may not port directly to the UK, EU, or other tax regimes where characterization, timing, and reporting rules differ materially.

Tax loss harvesting is a high-value operational discipline for crypto investors who have realized gains elsewhere or expect gains in the near term. Under current U.S. rules, crypto’s property classification enables TLH strategies that can materially lower tax liabilities, but their effectiveness depends on precise record-keeping, correct Form 8949/Schedule D reporting, and careful attention to regulatory evolution.

Use automated tax software to create audit-grade workpapers, sequence disposals intelligently to preserve holding-period tax advantages, and treat any immediate repurchases as policy decisions made with an eye toward possible future wash-sale-style rule changes.

If you follow a rigorous process, reconcile ledger data, execute clean taxable disposals, capture USD FMV and TXIDs, and produce Form 8949 entries, TLH can convert volatility into a reproducible tax asset that smooths realized-tax outcomes across years. For complex portfolios, involve tax counsel to align TLH execution with broader compliance programs.

Fill out a form and our bitcoin mining expert will contact you.

FREE CONSULTATIONFill out a form and our bitcoin mining expert will contact you.