Count me in!

Stay up to date with the latest news, announcements, and articles.

During the latest Blockchain Summit, Vice President J.D. Vance himself announced the new policies meant to ease both public and statewise adoption of crypto, Bitcoin in particular.

The optimistic crypto sentiment has culminated in the recent bill passing to enable first-ever fully regulated use of stablecoin currencies. GENIUS Act is the first in its kind stablecoin regulation issued officially by the U.S. Senate.

What does this mean for the BTC and crypto market in general? What are the key provisions of the bill? And how does it resonate across the community? Let’s take a look.

The bill in question is the G.E.N.I.U.S. Act — short for Guiding and Establishing National Innovation for U.S. Stablecoins Act, introduced documentally as S. 1582. Yes, you know what that means — we now have one of the first ever official backings of the state authority supporting crypto. Finally!

The GENIUS Act was passed by the Senate on June 17, 2025, with a 68–30 bipartisan vote, and then by the House on the same day (308–122). The bill was signed into law by President Trump on July 18.

Effectively, the bill establishes the first tangible federal framework for regulating stablecoins. Specifically, “payment stablecoins” — digital assets that can be redeemed for a fixed monetary value and designed to keep at a stable price.

The path towards Senate crypto approval was long and rough but steady. Some of the biggest decision-makers of the U.S. government seem to firmly believe in the regulated potential of digital coins.

With the latest tariff events, trade wars, and industry shifts, there were many moving factors to new Senate crypto policies. we can make out two main reasons why the U.S. Senate would favor stablecoin approvals right at this moment:

The newly-passed bill contains a number of provisions for legislating and regulating stable cryptos. You can read the full text of the US Stablecoin regulation bill 2025, but if we sum up, the core points and provisions described in it include the following:

There is a strict requirement for those issuing stablecoin payments — an issuer must be able to back the stablecoin with other liquid, low-risk assets in the one-to-one ratio (e.g., $1 of real assets for every $1 stablecoin issued). Such assets can be short-term US Treasuries, cash equivalents, T-bills, or regulated deposits that match the stablecoin’s value.

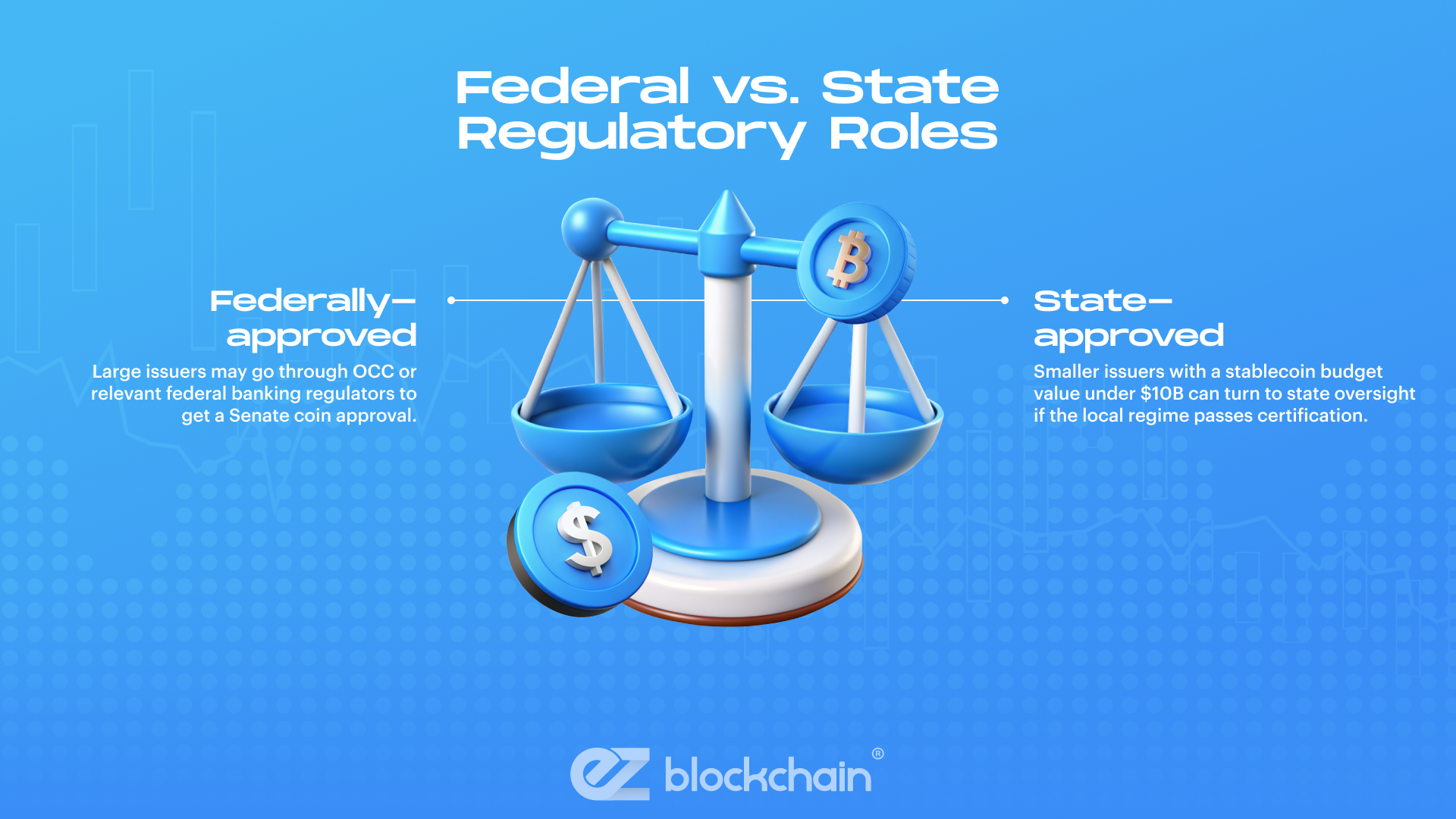

The first step in regulating the issuance of stablecoin is entitling the issuers. Only “permitted payment stablecoin issuers” get to issue stablecoins in the United States. These legal entities may include subsidiaries of federally-insured banks, nonbanks approved by the OCC, and particular issuers greenlit by the state (see more explanations below).

According to the US stablecoin regulation, payment stablecoins are explicitly not classified as securities, like gold or oil, or as commodities, like stocks and other CFTC. Instead, regulation is carried out by the federal bank regulators. This means that most stablecoins, especially those pegged to the US dollar, won’t be treated like investment products.

Issuers cannot offer stablecoin interest or yield to holders simply for holding stablecoins — no passive rewards are permitted by the GENIUS Act. This is regulated in order to diminish the speculative potential of stablecoins and make sure they function more as direct payment tools.

Issuers must publicly disclose their reserve holdings monthly, backed by independent third-party audits. CEOs and CFOs must certify these reports, and the larger the issuer, the more scrutiny and audit requirements they will have to face on a regular basis. Thanks to this, users will be able to verify the legitimacy of the issued stablecoins.

In the event an issuer goes bankrupt, the holders of their issued stablecoins are prioritized for refunds over all other creditors, even above secured or administrative claims. Reserves backing the stablecoins are also exempted from the issuer’s bankruptcy estate. All of this means it will become easier for the holders to retrieve their funds, making stablecoins overall safer to use.

Foreign stablecoin issuers can only operate in the US if their home nation has a regulatory regime that is approved as comparable by the U.S. Treasury. On top of that, they must register with US regulators, have US-based reserves, and comply with US law.

The provisions described in the US stablecoin regulation 2025 come into full lawful effect upon whichever comes first:

Note that cryptocurrency exchanges and services providers get an extended transition period until July 2028, gaining up to three years’ more time to become familiar with the new rules.

The new stablecoin law framework means new, better regulated realities for stable crypto traders, holders, investors, and other enthusiasts. However, the new law also narrows the range of entities that can issue stablecoins.

Only permitted payment stablecoin issuers aka PPSIs can legally issue stablecoins. These include:

While federal rules set the baseline regulations, individual states can step in for smaller issuers if their frameworks match the federal standards. A Stablecoin Certification Review Committee oversees this comparability.

This slight gap between the federal and state regulations opens two paths for issuing lawful stablecoins:

Some state licensing requirements are preempted for PPSIs, though consumer protection laws stay in place and will be enforced.

The stablecoin regulation US 2025 will certainly have a far-reaching effect, especially once it becomes fully lawfully active. The most impact will be felt by the companies working directly with crypto (e.g., exchanges, tracking platforms, service providers, etc.) and investors.

Namely, we all should expect:

On the downside:

Although we are yet to see the bigger waves set off by the new legislation, the first ripples are already abound. Taking a closer look at the industry and market state, here’s what we have on the agenda:

With the House’s approval and the President’s signature, the GENIUS Act is now law. Final rulemaking begins, but the full enforcement kicks in within 120 days post-regulation or 18 months from enactment.

If you want to timely prepare or launch a new crypto operation that complies with upcoming regulations, contact EZ Blockchain. We will consult your next steps and cover your tech needs.

Fill out a form and our bitcoin mining expert will contact you.

FREE CONSULTATIONFill out a form and our bitcoin mining expert will contact you.